Payables:

1. Complete All Transactions for the Period Being Closed

2. Run the Payables Auto Approval Process for All Invoices / Invoice Batches

3. Review & Resolve Amounts to Post to the General Ledger

4. Reconcile Payments to Bank Statement Activity for the Period

5. Transfer All Approved Invoices Payments, Reconciled Payments to the General Ledger

6. Review the Payables to General Ledger Posting Process After Completion

7. Submit the Unaccounted Transactions Sweep Program

8. Close the Current Oracle Payables Period

9. Accrue Uninvoiced Receipts

10. Reconcile Oracle Payables Activity for the Period

11. Run Mass Additions Transfer to Oracle Assets

12. Open the Next Payables Period

13. Run Reports for Tax Reporting Purposes (Optional)

14. Run the Key Indicators Report (Optional)

15. Purge Transactions (Optional)

Purchasing:

1. Complete All Transactions for the Period Being Closed

2. Review the Current and Future Commitments (Optional)

3. Review the Outstanding and Overdue Purchase Orders (Optional)

4. Follow up Receipts-Check with Suppliers

5. Identify and Review Un-invoiced Receipts (Period End Accruals)

6. Follow Up Outstanding Invoices

7. Complete the Oracle Payables- Period End Process

8. Run Receipt Accruals - Period End Process

9. Reconcile Accounts - Perpetual Accruals

10. Perform Year End Encumbrance Processing. (Optional)

11. Close the Current Purchasing Period.

12. Open the Next Purchasing Period.

13. Run Standard Period End Reports (Optional)

2. Review the Current and Future Commitments (Optional)

3. Review the Outstanding and Overdue Purchase Orders (Optional)

4. Follow up Receipts-Check with Suppliers

5. Identify and Review Un-invoiced Receipts (Period End Accruals)

6. Follow Up Outstanding Invoices

7. Complete the Oracle Payables- Period End Process

8. Run Receipt Accruals - Period End Process

9. Reconcile Accounts - Perpetual Accruals

10. Perform Year End Encumbrance Processing. (Optional)

11. Close the Current Purchasing Period.

12. Open the Next Purchasing Period.

13. Run Standard Period End Reports (Optional)

Inventory/WIP:

1. Complete All Transactions for the Period Being Closed.

2. Check Inventory and Work In Process Transaction Interfaces.

3. Check Oracle Order Management Transaction Process.

4. Review Inventory Transactions.

5. Balance the Perpetual Inventory.

6. Validate Work In Process Inventory.

7. Transfer Summary or Detail Transactions

8. Close the Current Oracle Payables and Oracle Purchasing Periods

9. Close the Current Inventory Period

10. Open the Next Inventory Period

11. Run Standard Period End Reports (Optional)

2. Check Inventory and Work In Process Transaction Interfaces.

3. Check Oracle Order Management Transaction Process.

4. Review Inventory Transactions.

5. Balance the Perpetual Inventory.

6. Validate Work In Process Inventory.

7. Transfer Summary or Detail Transactions

8. Close the Current Oracle Payables and Oracle Purchasing Periods

9. Close the Current Inventory Period

10. Open the Next Inventory Period

11. Run Standard Period End Reports (Optional)

Order Management:

1. Complete All Transactions for the Period Being Closed

2. Ensure all Interfaces are Completed for the Period (Optional)

3. Review Open Orders and Check the Workflow Status

4. Review Held Orders

5. Review Discounts

6. Review Backorders

7. Review and Correct Order Exceptions

8. Reconcile to Inventory

9. Reconcile to Receivables (Optional)

2. Ensure all Interfaces are Completed for the Period (Optional)

3. Review Open Orders and Check the Workflow Status

4. Review Held Orders

5. Review Discounts

6. Review Backorders

7. Review and Correct Order Exceptions

8. Reconcile to Inventory

9. Reconcile to Receivables (Optional)

10. Run Standard Period End Reports

Receivables:

1. Complete All Transactions for the Period Being Closed

2. Reconcile Transaction Activity for the Period

3. Reconcile Outstanding Customer Balances

4. Review the Unapplied Receipts Register

5. Reconcile receipts.

6. Reconcile Receipts to Bank Statement Activity for the Period

7. Post to the General Ledger

8. Reconcile the General Ledger Transfer Process

9. Reconcile the Journal Import Process

10. Print Invoices

11. Print Statements (Optional)

12.Print Dunning (Reminder) Letters (Optional)

13. Close the Current Oracle Receivables Period

14. Reconcile Posted Journal Entries

15. Review Unposted Items Report

16. Open the Next Oracle Receivables Period

17. Run Reports for Tax Reporting Purposes (Optional)

18. Run Archive and Purge programs (Optional)

2. Reconcile Transaction Activity for the Period

3. Reconcile Outstanding Customer Balances

4. Review the Unapplied Receipts Register

5. Reconcile receipts.

6. Reconcile Receipts to Bank Statement Activity for the Period

7. Post to the General Ledger

8. Reconcile the General Ledger Transfer Process

9. Reconcile the Journal Import Process

10. Print Invoices

11. Print Statements (Optional)

12.Print Dunning (Reminder) Letters (Optional)

13. Close the Current Oracle Receivables Period

14. Reconcile Posted Journal Entries

15. Review Unposted Items Report

16. Open the Next Oracle Receivables Period

17. Run Reports for Tax Reporting Purposes (Optional)

18. Run Archive and Purge programs (Optional)

Assets:

1. Complete All Transactions for the Period Being Closed

2. Assign All Assets to Distribution Lines

3. Run Calculate Gains and Losses (Optional)

4. Run Depreciation

5. Create Journal Entries

6. Rollback Depreciation and/or Rollback Journal Entries (Optional)

7. Create Deferred Depreciation Journal Entries (Optional)

8. Depreciation Projections(Optional)

9. Review and Post Journal Entries

10. Reconcile Oracle Assets to Oracle General Ledger Using Reports.

11. Run Responsibility Reports (Optional)

12. Archive and Purge Transactions (Optional)

2. Assign All Assets to Distribution Lines

3. Run Calculate Gains and Losses (Optional)

4. Run Depreciation

5. Create Journal Entries

6. Rollback Depreciation and/or Rollback Journal Entries (Optional)

7. Create Deferred Depreciation Journal Entries (Optional)

8. Depreciation Projections(Optional)

9. Review and Post Journal Entries

10. Reconcile Oracle Assets to Oracle General Ledger Using Reports.

11. Run Responsibility Reports (Optional)

12. Archive and Purge Transactions (Optional)

Projects:

1. Change the Current Oracle Projects Period Status from Open to Pending Close

2. Open the Next Oracle Projects Period

3. Complete All Maintenance Activities

4. Run Maintenance Processes

5. Complete All Transaction Entry for the Period Being Closed

6. Run the Final Cost Distribution Processes

7. Interface Transactions to Other Applications (AP, GL, FA)

8. Generate Draft Revenue for All Projects

9. Generate Invoices

10. Run Final Project Costing and Revenue Management Reports

11. Transfer Invoices to Oracle Receivables

12. Interface Revenue to General ledger (Project Billing Only)

13. Run Period Close Exception and Tieback Reports

14. Change the Current Period Oracle Projects Status from Pending Close to Closed

15. Advance the PA Reporting Period (Optional)

16. Update Project Summary Amounts

17. Restore Access to User Maintenance Activities

18. Permanently Close the Oracle Projects Period (Optional)

19. Reconcile Cost Distribution Lines with General Ledger (Optional)

2. Open the Next Oracle Projects Period

3. Complete All Maintenance Activities

4. Run Maintenance Processes

5. Complete All Transaction Entry for the Period Being Closed

6. Run the Final Cost Distribution Processes

7. Interface Transactions to Other Applications (AP, GL, FA)

8. Generate Draft Revenue for All Projects

9. Generate Invoices

10. Run Final Project Costing and Revenue Management Reports

11. Transfer Invoices to Oracle Receivables

12. Interface Revenue to General ledger (Project Billing Only)

13. Run Period Close Exception and Tieback Reports

14. Change the Current Period Oracle Projects Status from Pending Close to Closed

15. Advance the PA Reporting Period (Optional)

16. Update Project Summary Amounts

17. Restore Access to User Maintenance Activities

18. Permanently Close the Oracle Projects Period (Optional)

19. Reconcile Cost Distribution Lines with General Ledger (Optional)

Cash Management:

1. Load Bank Statements

2. Reconcile Bank Statements

3. Create Miscellaneous Transactions

4. Review AutoReconciliation Execution Report

5. Resolve Exceptions on the AutoReceonciliation Execution Report

6. Run Bank Statement Detail Report

7. Run Transactions Available for Reconcilaition Report

8. Resolve Un-reconciled Statement Lines

9. Run the GL Reconciliation Report

10. Run the Account Analysis Report for the General Ledger Cash Account

11. Review the Account Analysis Report

12. Correct any Invalid Entries to the General Ledger Cash Account (Optional)

13. Perform the Bank Reconciliation

2. Reconcile Bank Statements

3. Create Miscellaneous Transactions

4. Review AutoReconciliation Execution Report

5. Resolve Exceptions on the AutoReceonciliation Execution Report

6. Run Bank Statement Detail Report

7. Run Transactions Available for Reconcilaition Report

8. Resolve Un-reconciled Statement Lines

9. Run the GL Reconciliation Report

10. Run the Account Analysis Report for the General Ledger Cash Account

11. Review the Account Analysis Report

12. Correct any Invalid Entries to the General Ledger Cash Account (Optional)

13. Perform the Bank Reconciliation

General Ledger:

1. Ensure the Next Accounting Period Status is Set to Future Entry

2. Complete Oracle Sub-ledger Interfaces to Oracle General Ledger

3. Upload Journals from ADI (Applications Desktop Integrator) to Oracle General Ledger

4. Complete Non-Oracle Sub-ledger Interfaces to Oracle General Ledger (Optional)

5. Generate Reversal Journals (Optional)

6. Generate Recurring Journals (Optional)

7. Generate Mass Allocation Journals (Optional)

8. Review and Verify Journal Details of Unposted Journal Entries

9. Post All Journal Batches

10. Run General Ledger Trial Balances and Preliminary Financial Statement Generator Reports (FSGs)

11. Revalue Balances (Optional)

12. Translate Balances (Optional)

13. Consolidate Sets of Books (Optional)

14. Review and Correct Balances (Perform Reconciliations)

15. Enter Adjustments and / or Accruals and Post

16. Perform Final Adjustments

17. Close the Current Oracle Gneral Ledger Period

18. Open the Next Oracle General Ledger Period

19. Run Financial Reports for the Closed Period

20. Run Reports for Tax Reporting Purposes (Optional)

21. Perform Encumbrance Year End Procedures (Optional)

2. Complete Oracle Sub-ledger Interfaces to Oracle General Ledger

3. Upload Journals from ADI (Applications Desktop Integrator) to Oracle General Ledger

4. Complete Non-Oracle Sub-ledger Interfaces to Oracle General Ledger (Optional)

5. Generate Reversal Journals (Optional)

6. Generate Recurring Journals (Optional)

7. Generate Mass Allocation Journals (Optional)

8. Review and Verify Journal Details of Unposted Journal Entries

9. Post All Journal Batches

10. Run General Ledger Trial Balances and Preliminary Financial Statement Generator Reports (FSGs)

11. Revalue Balances (Optional)

12. Translate Balances (Optional)

13. Consolidate Sets of Books (Optional)

14. Review and Correct Balances (Perform Reconciliations)

15. Enter Adjustments and / or Accruals and Post

16. Perform Final Adjustments

17. Close the Current Oracle Gneral Ledger Period

18. Open the Next Oracle General Ledger Period

19. Run Financial Reports for the Closed Period

20. Run Reports for Tax Reporting Purposes (Optional)

21. Perform Encumbrance Year End Procedures (Optional)

Payment Netting

Payment Netting

Novation Netting

Novation Netting

Close-Out Netting

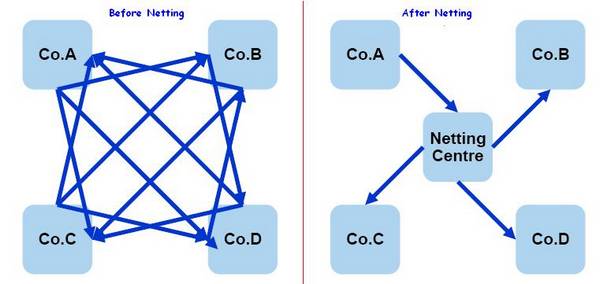

Close-Out Netting Multilateral Netting

Multilateral Netting